Many dentists know by instinct and experience when their busiest months of the year are - and perhaps even why.

But a newly issued study of 2.3 million Americans, conducted by The JPMorgan Chase Institute, uses hard data to validate the intuition of dentists, and permits them to compare how their patient base matches up with other practices statewide and nationwide.

Insights gleaned from the study, the first-ever of its kind, will help empower dental practice managers and savvy dental marketers to address questions such as:

- What are the best and worst times of the year to market to new and existing patients?

- In what month should you plan doctor or staff vacations?

- What percentage of their annual income will most patients spend on healthcare generally, and dentistry more specifically?

- How does the state or region in which a dentist practices impact consumer healthcare spending?

The study, formally titled the JPMorgan Chase Institute Healthcare Out-of-Pocket Spending Panel (JPMCI HOSP), zeroes in on direct consumer spending on healthcare, not counting insurance-paid benefits and reimbursements.

The study, formally titled the JPMorgan Chase Institute Healthcare Out-of-Pocket Spending Panel (JPMCI HOSP), zeroes in on direct consumer spending on healthcare, not counting insurance-paid benefits and reimbursements.

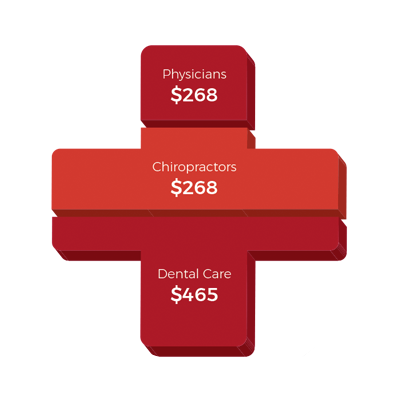

What JPMCI HOSP found is that 21% of total consumer out-of-pocket healthcare spending goes for dental care, just shy of the 22% that patients spend on their physicians. No other out-of-pocket healthcare expenditures - not even on hospitalization - comes close.

In fact, consumers reach deeper into their pockets to buy dental care than they do for any single health-related category, including physicians, hospitals, chiropractors, pharmacies, and home health services.

[What It Means: The dental profession can be proud that it has merited the broad trust of consumers to the extent that they regularly visit their dentist and prioritize their oral health over other discretionary healthcare spending.]

On average, based on outlays tracked by consumers utilizing Chase credit and debit cards, and Chase electronic bill pay, the average family spent $465 of their own funds in 2016 (the most recent year available) on dental care compared with $293 on physicians and $268 on chiropractors.

While all spending on healthcare in 2016 rose by an average of 4.3%, as a percentage of take-home income, out-of-pocket spending on healthcare remained constant at 1.6% of disposable income.

Women spent a larger portion of their take-home pay on healthcare than did men, and understandably - because most healthcare fees are not indexed to a patient's income - those who earned the least expended the largest percentage of their income on healthcare when compared to those who earned the most.

[What It Means: It's easier for upper-middle-class and wealthy patients to self-fund extensive dental restoration and cosmetic work than it is for lower-middle-class and low-income patients to afford basic dental services.]

The biggest out-of-pocket healthcare spenders, representing 10% of all those tracked by JPMCI HOSP, accounted for a whopping 49% of total out-of-pocket healthcare expenses. These patients, out of choice or necessity, paid out 9% of their take-home pay on healthcare. (Keep in mind that the dental profession and physicians each receive the largest portion of patient out-of-pocket spending.)

Moreover, JPMCI HOSP's analyses discovered that March, April, October, and December are months when consumers spend more on healthcare than the rest of the year.

"Families made larger healthcare payments in the months when they had a higher ability to pay," the study's authors observed. Indeed, JPMorgan Chase knows quite assuredly when during the year "deposits" reach their peak, so it can report with confidence the high correlation between income, liquid assets, and healthcare spending.

This portion of the JPMCI HOSP study, alone, might cause many dental practice managers and dental marketers to rethink their current outreach strategies.

What It Means:

- Oral health care is among the "discretionary spending" priorities that consumers set for themselves, when their take-home income rises. A buoyant economy and low-unemployment numbers will send more consumers to their dentists.

- The best time to attract new patients and encourage existing patients to begin discretionary cosmetic and restorative treatments is March, April, October, and December. (Tax refunds - March and April - and year-end bonuses - December - are two of the reasons consumers have more funds to spend in these months. October's blip may relate to the open enrollment period for health insurance.)

Obviously, marketing campaigns are more likely to succeed when they are planned ahead of time to coincide with months when patients are most "flush."

These four months, generally*, would be the wrong time for dentists or team members to take vacations. They likely would be an excellent time to bring on "seasonal" support personnel. - The worst time to try to attract new patients, or reactivate existing patients, is June, when JPMCI HOSP reports that it's banking customers show the least month-to-month take-home pay.

Likewise, June appears to be the best time* for many dentists and team members to take their annual vacations.

(*Obviously, dentists must take into account their unique practice demographics. In some regions, and for some patients - such as kids on summer vacation - June might be a perfect month to attract and treat new patients.)

Most established dentists have little flexibility when it comes to the state or region where they are located. (Dental school students, on the other hand, may want to take careful notice of the JPMCI HOSP study before deciding where to locate upon graduation.)

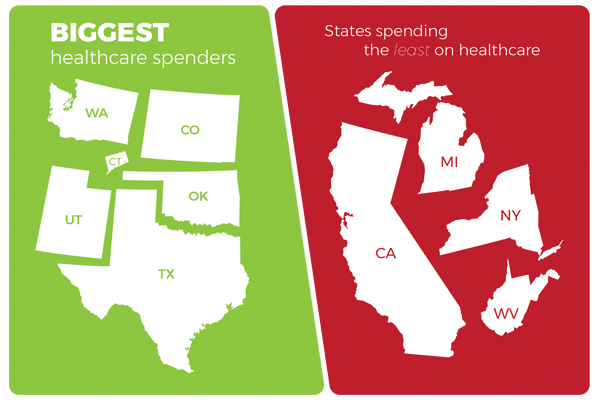

Nonetheless, for established dentists, it's good to know when you read or hear about how much a dentist in another part of the country charges for his or her services - and it's significantly more than you ask - that out-of-pocket healthcare spending varies dramatically depending on geography.

On the whole, residents in Colorado, Utah, Connecticut, Texas, Oklahoma, and Washington are the biggest spenders when it comes to their healthcare. Consumers in New York, Michigan, West Virginia, and California, on average, spend considerably less.

JPMCI HOSP, of course, can't accurately reflect how any single state, city, or county will behave - nor for that matter, is it an accurate measure of how any single dental practice should or will perform. Innumerable other factors - including the dentist's reputation and talent, customer service, marketing, and pricing - will impact the dentist's bottom line.

But JPMCI HOSP offers a data-rich benchmark for dentists and their team members to utilize in measuring their practice performance. Even minor adjustments, in the timing of patient-acquisition campaigns, for example, may make a world of economic difference.

[To download a free copy of the JPMCI HOSP report, click here.]

The information contained in this, or any case study post in Incisor should never be considered a proper replacement for necessary training and/or education regarding adult oral conscious sedation. Regulations regarding sedation vary by state. This is an educational and informational piece. DOCS Education accepts no liability whatsoever for any damages resulting from any direct or indirect recipient's use of or failure to use any of the information contained herein. DOCS Education would be happy to answer any questions or concerns mailed to us at 106 Lenora Street, Seattle, WA 98121. Please print a copy of this posting and include it with your question or request.